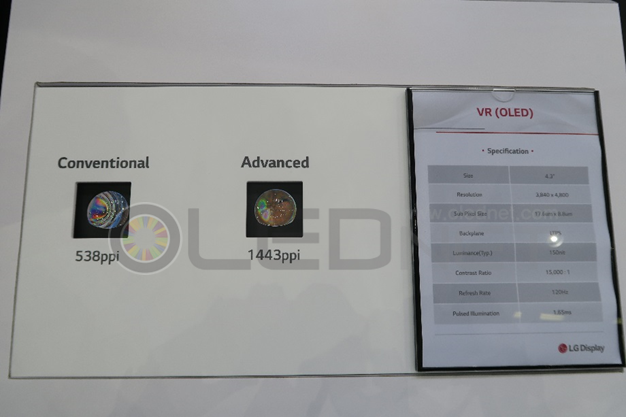

Samsung Display, 프리미엄 노트북 시장 출사표

Samsung Display가 세계 최초로 UHD 해상도의 노트북용 OLED 디스플레이를 개발, 프리미엄 IT시장 공략에 적극 나선다.

Samsung Display는 23일 15.6형 크기의 UHD(3840 x 2160) OLED를 개발했으며, 2월부터 양산에 들어가 글로벌 노트북 제조사에 공급할 예정이라고 밝혔다. 이 제품은 초고해상도 기술을 바탕으로 게이밍, 그래픽 디자인, 동영상 감상 등에 특화된 프리미엄 화질을 구현한다.

<Source: Samsung Display>

Samsung Display가 개발한 OLED 패널은 명암비, 색정확도, HDR, 광색역, 야외시인성 등 프리미엄 노트북에 필수적인 기능을 갖추고 있다.

이 제품의 밝기는 최저 0.0005니트(nit)에서 최고 600니트(nit)로 120만대 1의 명암비를 갖췄다. LCD와 비교해 블랙은 200배 어둡게, 화이트는 2배 이상 밝게 표현할 수 있다. 이는 고화질의 동영상 및 이미지 감상에 필수적인 HDR을 극대화한다.

또한 OLED가 보유한 3400만개의 색상 (LCD 대비 2배이상 많음)을 바탕으로 동영상 재생의 최적 색 기준인‘DCI-P3’를 100% 충족해 실제에 가장 근접한 색상을 구현한다. 특히 안구에 유해하다고 알려진 블루라이트를 LCD 대비 현격하게 줄여서 이용시간이 긴 노트북 사용자들의 시력보호에도 기여한다.

노트북 컴퓨터는 PC와 달리 이용환경이 수시로 바뀌어 주변 밝기 변화가 빈번하다. 삼성디스플레이의 15.6형 OLED 패널은 LCD대비 1.7배 높은 컬러볼륨으로 야외에서도 화질 저하를 줄여 시인성을 대폭 높였다. 또 LCD 대비 얇고 가벼운 구조적 특성과 저소비 전력의 강점은 노트북 휴대의 편의성을 극대화했다.

<Source: Samsung Display>

윤재남 Samsung Display 마케팅팀장은 “Samsung Display의 15.6형 OLED는 압도적인 HDR과 뛰어난 색 재현력, 높은 야외 시인성 등 휴대용 IT 기기에 최적화된 디스플레이 솔루션을 제공한다”면서“기존 노트북 시장이 본체 기능에 집중했다면 향후 소비자들은 OLED 노트북을 통해 한 차원 높은 시각 경험까지 누릴 수 있을 것”이라고 강조했다.

한편, Samsung Display의 15.6형 OLED는 미국 비디오 전자 공학 협회(VESA)가 인정한 True Black을 실현했다. VESA는 최근 신규표준인 ‘DisplayHDR TrueBlack’을 발표하면서 이는 기존 HDR 표준대비 100배 깊은 블랙레벨을 표현하는 것으로 삼성이 이 표준을 통과했다고 밝혔다. ‘DisplayHDR TrueBlack’은 실제 사람이 눈으로 보는 것에 근접하게 어두운 곳은 더욱 어둡게, 밝은 곳은 더욱 밝게 구현해 한단계 높은 HDR을 제공한다는 의미다.

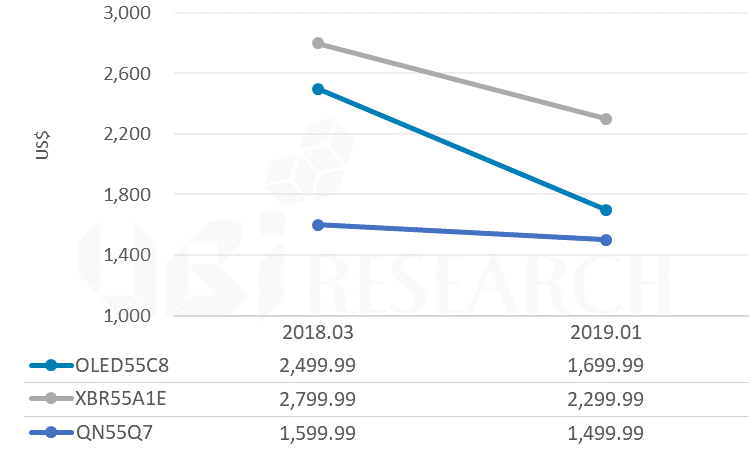

<55 inch 프리미엄 TV 가격 비교>

<55 inch 프리미엄 TV 가격 비교>

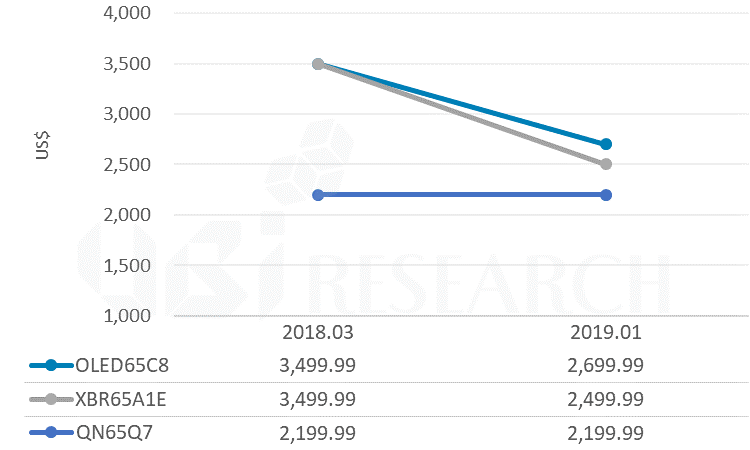

<엘지전자, OLED TV R>

<엘지전자, OLED TV R>

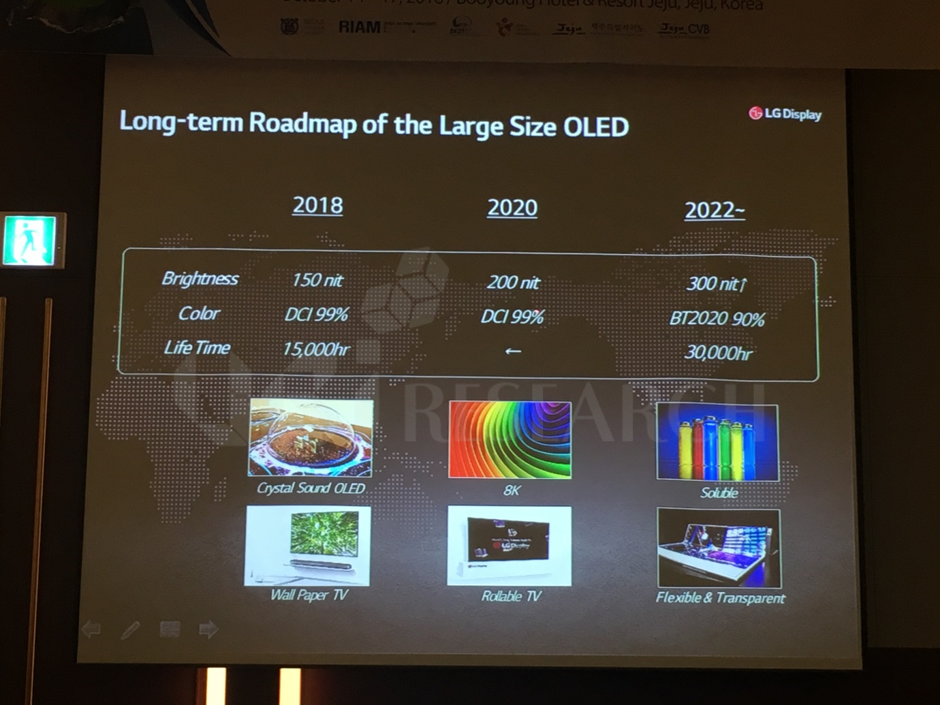

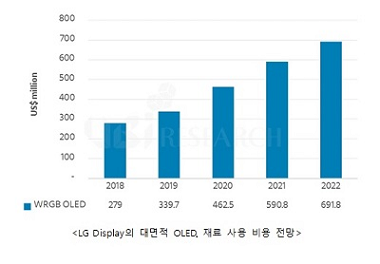

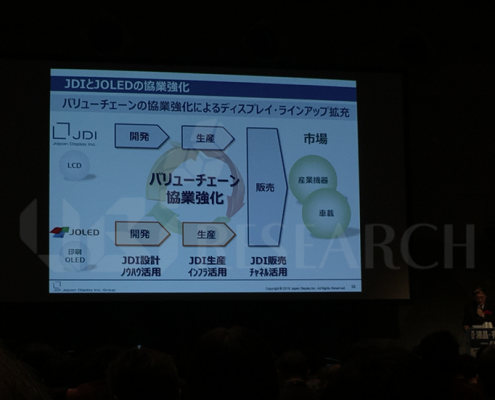

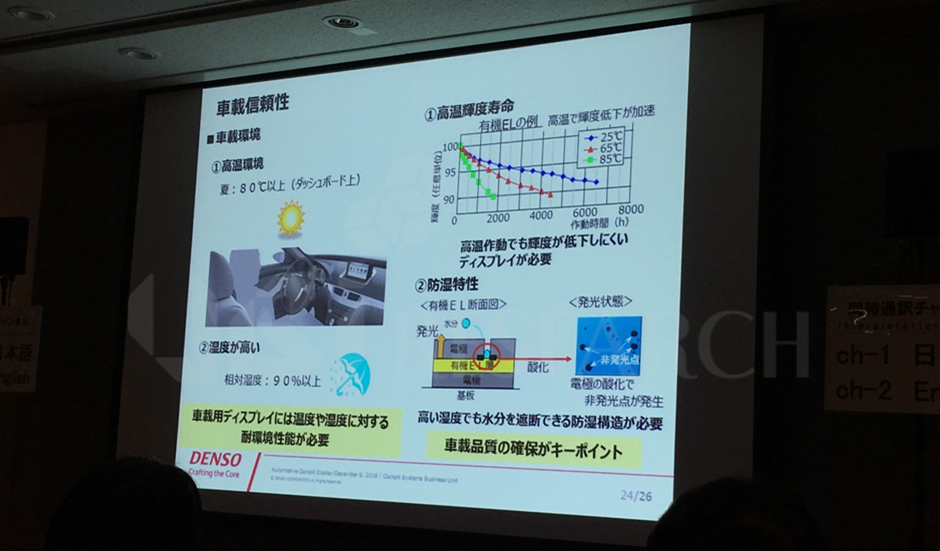

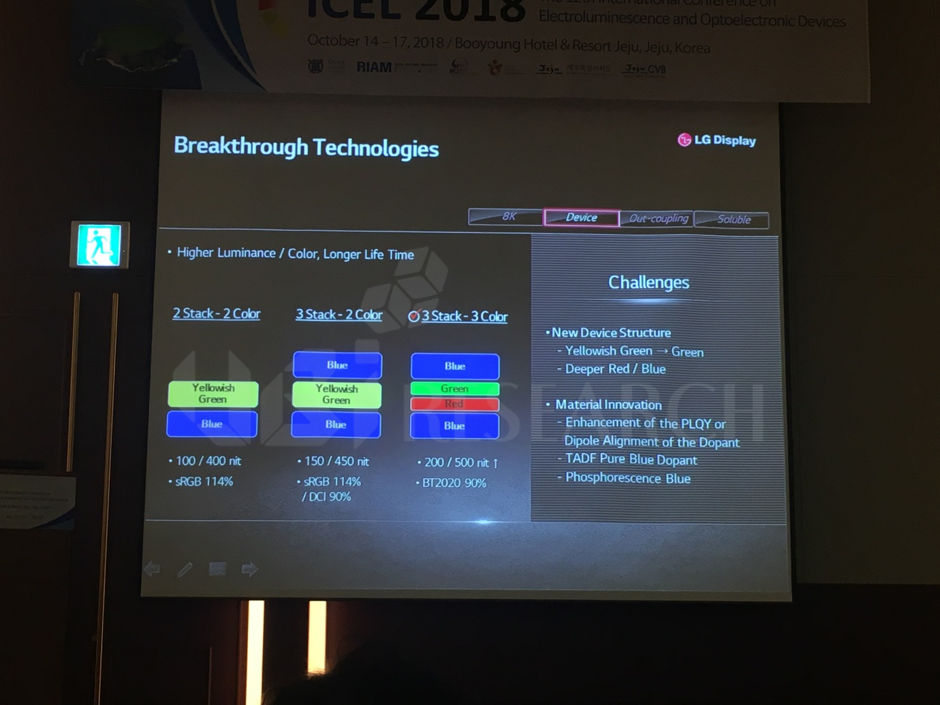

또한, LCD TV 가격에 대응하기 위한 기술로 solution process OLED를 언급하며 잉크젯 장비와 공정, soluble 재료의 개발도 필요하다고 밝혔다. 이를 위해서는 잉크젯 장비 개발과 대량 생산을 위한 공정 시간 단축도 필요하지만, soluble 재료의 성능과 신뢰성이 무엇보다도 중요할 것이라 언급했다.

또한, LCD TV 가격에 대응하기 위한 기술로 solution process OLED를 언급하며 잉크젯 장비와 공정, soluble 재료의 개발도 필요하다고 밝혔다. 이를 위해서는 잉크젯 장비 개발과 대량 생산을 위한 공정 시간 단축도 필요하지만, soluble 재료의 성능과 신뢰성이 무엇보다도 중요할 것이라 언급했다.